")

Akropolis is an Ethereum-based protocol that provides financial services to the informal economy.

Most decentralized finance (DeFi) platforms concentrate on a subset of yield farming or liquidity mining at the top of their menu. This aspect deals with mostly lending and borrowing services, leaving savings, which is also a crucial part of a decentralized financial ecosystem, unattended or not fully developed.

Although projects have attempted to close this gap, Akropolis aims to do a better job. Generally, Akropolis flips conventional finance to introduce a fully DeFi-structured world.

Table of Contents

Background

Akropolis is inspired by conventional financial systems that have morphed over time to achieve their current functionalities. However, a key concept of these systems is to better the realization of peoples’ financial needs.

Banks have remained at the center of these systems. Unfortunately, not everyone owns or has access to a bank account, especially those living in informal settings. In here, chamas or saving circles power informal financial firms. With these platforms being centralized, users are still prone to losing their funds when these firms wind up inoperational, sometimes without notice.

Akropolis works to mitigate these risks by offering a decentralized platform with the same functionalities as a centralized informal financial organization.

What is Akropolis?

Akropolis is an Ethereum-based protocol that provides financial services to the informal economy. It powers a bankless ecosystem where users can issue a credit, insure, or save without lying on a central authority such as a bank. Its users can be individuals, cooperatives, or community groups such as saving circles.

For those interested in yield farming or liquidity mining, the platform is integrated with the leading yield farming protocols such as Compound, Aave, Curve, and Yearn. However, the network has two DeFi-focused products called Sparta and Delphi. Sparta enables access to undercollateralized loans, while Delphi allows automated passive investing.

The platform is made up of end-users, autonomous finance organizations (AFOs), capital providers, and network keepers.

End-users

End-users can save and receive rewards on their savings, as well as receive loans. Furthermore, gaining interest from their savings incentivizes them to deposit their money with AFOs.

AFOs

These are borrowers plus their associations. They receive credit at a fair interest rate. Their work is to make the credit easily available by providing a reasonable price and enhance the terms of credit. Existing AFOs earn rewards by inviting more AFOs onto the platform. The Akropolis network also has private AFOs that activate a private status when dealing with user savings.

Capital providers

Also called lenders, they give loans by evaluating the risk and profit margins among those that seek capital. The network connects lenders and AFOs efficiently in order to prevent and/or eradicate loan defaults.

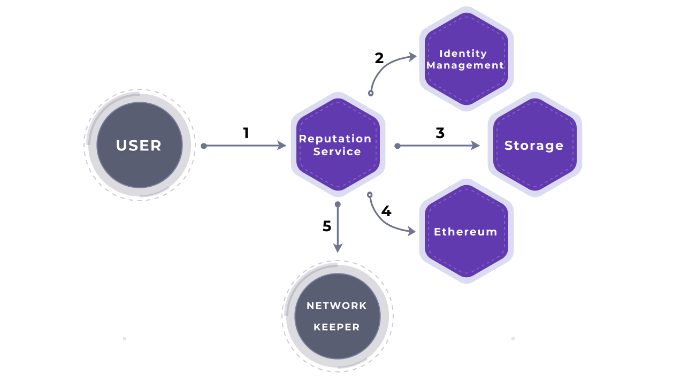

Network keepers

Network keepers provide risk assessment, and are rewarded with the system’s native tokens (more on this later) stored in a growth fund.

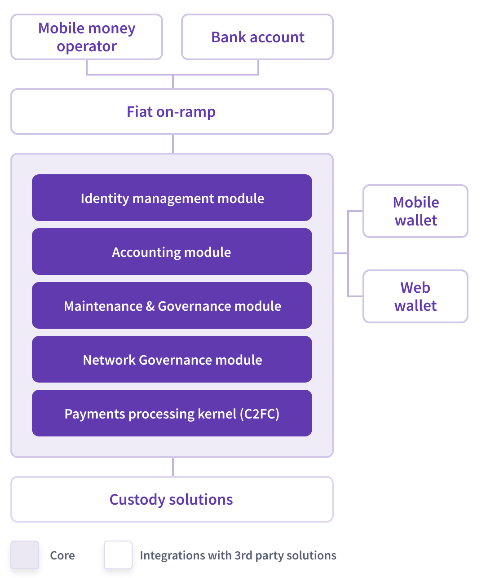

How Akropolis works

The protocol is structured in layers, with each of them handling a specific function. Major layers include:

Identity Management (IM) module

With most distributed projects using a decentralized autonomous organization (DAO) to provide community engagement in decision making, there still lacks a single entry point for membership management. The Akropolis IM module provides a single entry access to all AFOs where a user has a membership. Think of Facebook; only one account is required to access groups and pages. Here a Facebook account serves as a single entry point to groups and pages.

Information created and kept by the IM module include:

· The number of AFOs on the network.

· A registry with all users.

· A link to users’ additional information stored on external platforms.

· A list of all AFO members.

Payment Processing Kernel

The system uses what it calls ‘Commitments to Future Cash Flows (C2FC)’ that converts a transaction on the network into a tokenized cash flow. With C2FC, the network powers a smooth batching, transfer, trading, or transfer of cash flows regardless of the issuer.

An issuer can be an individual, a DAO, machine, or corporate. Financial interactions between, for instance, lenders and borrower is recorded as a cash flow exchange.

C2FC’s core functions are creating cash flow, payment execution, and payment withdrawal.

Network Governance Module (NGM)

Through an application programming interface (API), the governance framework allows for the registration of financial firms, the addition of new users, and the distribution of profits. Additionally, NGM allows for the exchange of assets on the platform and lending of funds between AFOs.

However, the actual governance of the Akropolis network is done by its members who hold the platform’s native tokens. Voters decide on governance fees, stability fees, intra-network loan rates, and penalty fees.

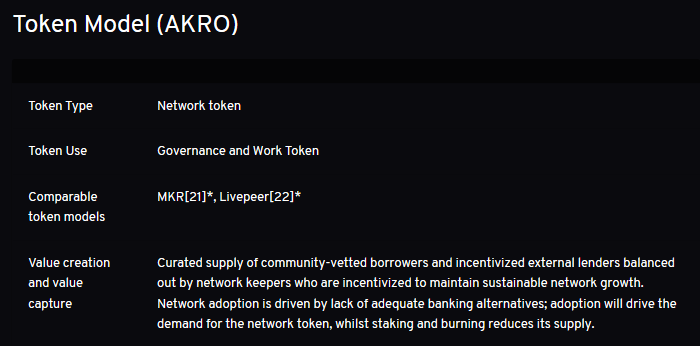

The Akrapolis token (AKRO)

Akropolis’ native currency is called AKRO. Its value creation and capture are based on trusted borrowers and lenders. AKRO is used as a governance and work token. For example, its holders have a right to contribute to the network and also have their voice heard on matters such as the platform’s design.

AKRO can also be used for staking and earning rewards in the process. Staking is the process of locking tokens in a wallet to power protocol activities. When using AKRO to provide liquidity, disbursement and repayment of loans is done using popular stablecoins. However, staking rewards are distributed using the native token.

The token’s value depends on its usage on the network. Activities that increase its worth include staking and voting.

In addition, AKRO’s design is inspired by MakerDAO’s framework.

Akropolis and Polkadot

To bring the newest internet version, Web 3.0, to the ecosystem, Akropolis works with Polkadot to further the project’s decentralization aspect. Through their partnership, Akropolis can provide a secure option, in case legacy financial systems collapse.

To benefit from Polkadot’s robustness, the protocol operates as a parachain on the platform and runs a validator node. Also, Akropolis’ Polkahub platform enables easy node deployment.

Conclusion

Although DeFi is a crucial part of non-custodial finance, Akropolis has added a software development kit (SDK) for those looking to upgrade their for-profit DAOs. Also, it has incorporated a save and earn feature that incentivizes users to interact with interest-based saving.

With a focus on the informal banking sector, the project can make a difference for the unbanked. For yield farmers, integration with popular platforms such as Compound, Curve, and Aave secures their place on the ecosystem.

/(CBDC) Guide")