")

The missing link between decentralized finance (DeFi) and centralized finance (CeFi) is that the former interacts only with cryptocurrencies such as Tether (USDT) and Bitcoin (BTC). In contrast, conventional finance mostly deals with fiat.

Although it’s easy to convert fiat to crypto, using real-world assets as collateral on DeFi platforms is not. What if there was a way to use real-world assets as collateral on these platforms? This is what the Persistence Protocol is trying to achieve.

This platform allows the use of tangible assets to access loans and returns on DeFi networks. To get a clear picture of how it’s possible, let’s dismantle and repackage Persistence.

Table of Contents

What is Persistence Protocol?

Initially, the project’s vision was to smoothen the remittances journey by interfacing DeFi and traditional finance. This vison also including relooking at business financing models. However, along the way, Persistence saw a need to inject fresh capital into the virtual currency world.

This was followed by a way for traditional borrowers to access open finance (OpFi) platforms and incur loans using invoices, inventory, property, and accounts receivables as collateral.

The blockchain-based project seeks to shift borrowers from the negative interest rates offered by some central banks and economies globally. For context, a negative interest rate produces losses instead of yields. In line with this, the project’s vision is achieved using NFTs (Non-Fungible Tokens) to represent invoices and other real-world assets, and then trading these NFTs in exchange for USDT and other stablecoins.

Furthermore, NFTs are used to originate loans and put the loans into pools to create debt securitization. Activities on the decentralized platform are powered by the Persistence token called XPRT.

The Problem With the Current Setup

Large corporations access financing with ease because they have enough resources (collateral needed). Small and medium-sized enterprises (SMEs), on the other hand, have little collateral to help them get funding VC firms and other financial providers.

This has been aggravated further by the hard rules imposed on banks and other financial institutions after the great financial crisis that rocked the world in 2008. As a result, a $1.5 trillion financing gap was created. Even if SMEs get loans, geographical boundaries can still get in the way of accessing global financing.

Other problems in the traditional financial sector are:

Delayed Cross-border payments

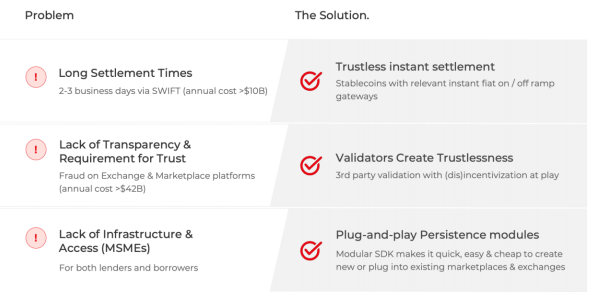

Even if SMEs get hold of global financing, the settlement times are considerably long, between 2-3 days. It needs to be noted that $10 billion is lost each year due to such long settlement times.

Low Trust and Transparency

Financial declarations from marketplaces, e-wallets, and centralized exchanges are vague, which raises transparency issues. Without transparency, auditors are forced to verify solvency reasons, among other issues where users may lose deposited or invested funds. This is exacerbated by the fact that most of the time, the audits are also trustworthy.

A gap Between SMEs and Investors

In the recent past, investors were gravitating towards SME financing. Unfortunately, there were no solid infrastructures for such an engagement causing SMEs to turn to peer-to-peer (P2P) lending. Unfortunately, P2P centralization also limits credit access and availability.

DeFi’s Here, but no Adoption As hoped. Why?

Blockchain-based Tokens Are the Only Tickets

Tangible assets in the traditional world are the ticket to credit. This includes bills of landing/exchange, or even a house under a mortgage can still be used as collateral. Unfortunately, DeFi does not recognize these valuable assets, which creates a gap.

Cryptocurrency Is Still a Foreign Concept

In the traditional world, cryptocurrencies are still considered extremely speculative assets for SMEs. And regulatory issues around this digital asset class make it even worse. Furthermore, crypto risks and acquisitions put another obstacle in cryptocurrency adoption by these small companies.

Data Safety

In this digital world, data safety and privacy is a major concern. With a lack of vital data controls to guard against leaks and malicious access, it hinders DeFi platforms from reaching their required adoption. Also, institutional adoption of OpFi is impeded by the public nature of decentralized platforms, where everyone has access to data.

The Persistence approach

The network has two methods: asset-based lending and pooling of debt.

Asset-based Lending

This deals with lenders who allow invoices, inventory, etc., to be used as collateral. Asset-based lending on the protocol is powered by Comdex, a decentralized platform that powers commodities trading.

Essentially, Comdex connects commodities buyers with physical commodities sellers. The platform has already handled more than $10 million in commodity trades.

Pooling of Debt (Securitization of Debt)

The pooling of debt involves an asset originator merging cash-flow generating assets to form an asset pool or pools. Consequently, interest is generated from the combined assets. Persistence has an ecosystem where a financier can handle multiple loans on the Comdex platform and keep invoices as collateral.

Based on risk levels, primary financiers, and other factors, these debts are classified into pools. The project then uses a dApp to allow stablecoin holders to provide liquidity to the pools and yield returns.

Persistence Token and Chain

To power communications with other blockchain-based platforms, Persistence uses inter-blockchain communication (IBC) protocols.

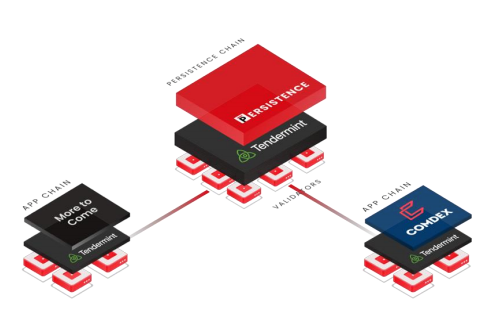

Persistennce Main Chain

To bring its vision to life, the project has a stack where the Persistence Chain serves as the core of its debt marketplace and software development framework that allows institutions to build and operate applications.

The Persistence main-chain uses a dPoS (delegated proof-of-stake) consensus mechanism with security provided by decentralized validators. However, depending on the business model, app chains can have customized security measures.

Persistence App Chains

The Persistence protocol also hosts “App-chains” that run application-specific logic. They are business-oriented and secured by the network’s main chain.

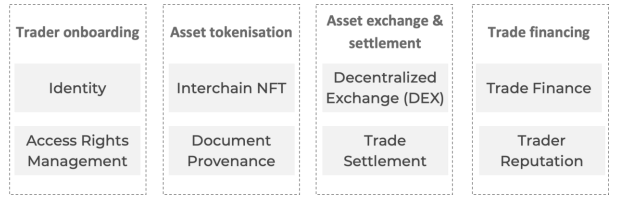

The SDK layer of the stack enables, among other things, an effortless way to connect to marketplaces and exchanges. Retail and institutional finance-focused applications are placed on the Persistence dApp layer.

Persistence SDK

The protocol’s software development kit (SDK) is a set of tools that are utilized in modeling marketplaces to facilitate the exchange of value. They can easily be fused with existing dapps. As a bonus, the SDK can also be utilized in different permutations and blends to come up with entirely new marketplaces.

Persistence DApps

OpFi dApps mainly deal with matching borrowers with investors or lenders, and run on app-specific chains in the protocol. Persistence intends to access both crypto and institutional liquidity at a the dApp layer by:

- offering institutional solutions powered by public blockchain technology, which would allow new capital to enter the cryptosphere by tapping into liquidity coming from institutions;

- offering crypto stakeholders institutional products by tapping into crypto liquidity, which would also give new opportunities to generate high returns once the stablecoin market stabilizes and yields become lower.

Conclusion

For institutional investments to flow into the cryptocurrency sector, traditional institutions need to be comfortable with these digital assets. This comfort can come from trusted platforms like Persistence bridging the gaps between these two worlds. Furthermore, interfacing crypto assets with real-world assets is the key to financing SMEs that have long been overshadowed by large corporations in terms of access to loans.

This will be made possible by lowering or eliminating the barrier to holding virtual currencies and embracing decentralized protocols that adequately address data privacy and security concerns. Persistence effectively tackles these problems using a stack made of app chains, SDK, dApps, and Persistence token (XPRT) to complete the cycle.

/(CBDC) Guide")