")

On 14 June, Binance announced that it “constantly reviews user accounts to improve (their) platform security and to comply with global compliance requirements”, mentioning that “Binance is unable to provide services to any U.S. person” in the latest “Binance Terms of Use” attached within the announcement.

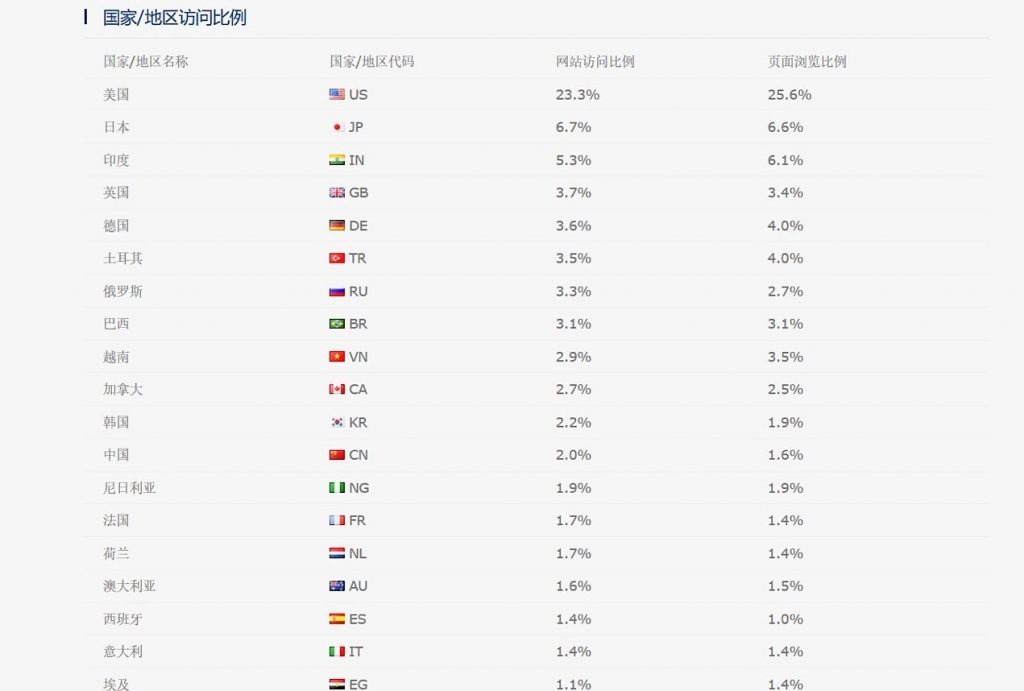

According to the data from a third-party traffic statistics website, Alexa, users in the U.S. form the biggest user group of Binance, accounting for about 25% of the total visitor traffic.

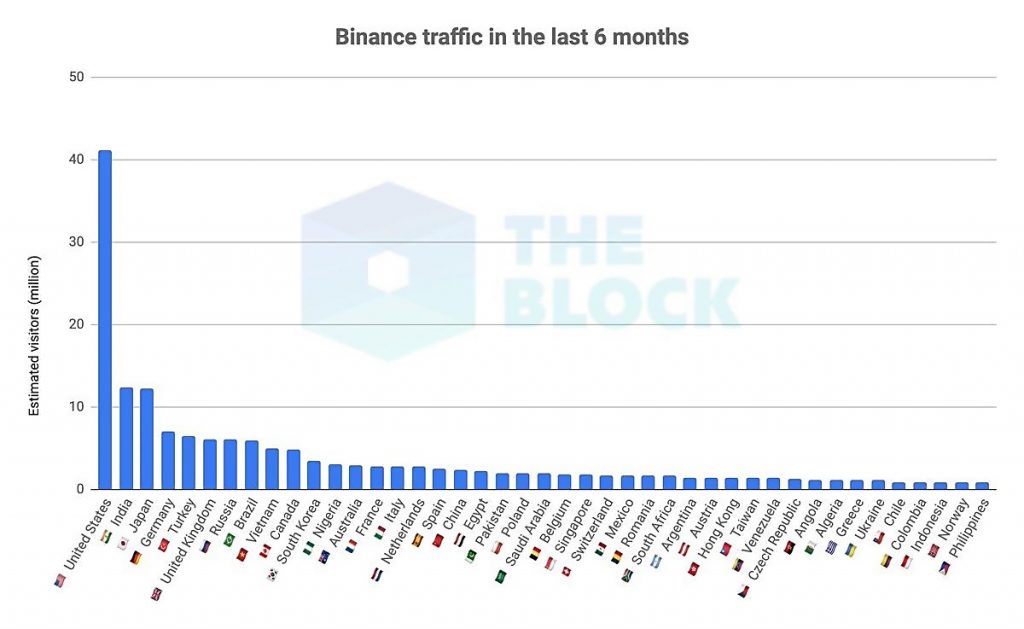

In the forecast of Binance’s user scale compiled by The Block, the largest traffic is dominated by users in the U.S., surpassing the total of the ones from the second place to the fifth place.

Also, considering that the scale of digital asset trading for the users in the U.S. far exceeds that of the users of many other countries, it could mean that Binance may have already lost 50 % of the business income by losing users in the U.S. Apparently, such an announcement by Binance to stop providing services to users in the U.S. means Binance has no other alternative but “seek to live on.”

So, what are the specific requirements of the U.S. for digital asset exchanges and which of the regulatory red lines of the U.S. did Binance cross?

- Compliance issues relating to operation permission of digital asset exchanges

In the U.S., the entry barrier for obtaining a business license to operate a digital asset exchange is not high. Apart from the special licencing requirements of individual states such as New York, most of the states generally grant licences to digital asset exchanges through the issuance of a “Money Transmitter License” (MTL).

- Each state has different requirements for MTL applications. Some of the main common requirements are:

- Filling out the application form, including business address, tax identification number, social security number and statement of net assets of the owner/proprietor

- Paying the relevant fees for the licence application

- Meeting the minimum net assets requirements stipulated by the state

- Completing a background check

- Providing a form of guarantee, such as security bonds

It is worth noting that not all states are explicitly using MTL to handle the issues around operation permission of digital asset exchanges. For instance, New Hampshire passed a new law on 12 March 2017, announcing that trading parties of digital assets in that state would not be bound by MTL. Also, Montana has not yet set up MTL, keeping an open attitude towards the currency trading business.

- On top of obtaining the MTL in each state, enterprises are also required to complete the registration of “Money Services Business” (MSB) on the federal level

FinCEN (Financial Crimes Enforcement Network of the U.S. Treasury Department) issued the “Application of FinCEN’s Regulations to Persons Administering, Exchanging, or Using Virtual Currencies” on 18 March 2013. On the federal level, the guideline requires any enterprise involved in virtual currency services to complete the MSB registration and perform the corresponding compliance responsibilities. The main responsibility of a registered enterprise is to establish anti-money laundering procedures and reporting systems.

However, California is an exception. Enterprises in California would only need to complete the MSB registration on the federal level and they do not need to apply for the MTL in California.

- Any enterprise operating in New York must obtain a virtual currency business license, Bitlicense, issued in New York

Early in July 2014, the New York State Department of Financial Services (NYSDFS) has specially designed and launched the BitLicense, stipulating that any institutions participating in a business relevant to virtual currency (virtual currency transfer, virtual currency trust, provision of virtual currency trading services, issuance or management of virtual currencies) must obtain a BitLicense.

To date, the NYSDFS has issued 19 Bitlicenses. Among them includes exchanges such as Coinbase (January 2017), BitFlyer (July 2017), Genesis Global Trading (May 2018) and Bitstamp (April 2019).

Solely from the perspective of operation permission, Binance has yet to complete the MSB registration of FinCEN (its partner, BAM Trading, has completed the MSB registration). This means that Binance is not eligible to operate a digital asset exchange in the U.S. FinCEN has the rights to prosecute Binance based on its failure to fulfil the relevant ‘anti-money laundering’ regulatory requirements.

- Compliance issues relating to online assets

With the further development of the digital asset market, ICO has released loads of “digital assets” that have characteristics of a “security” into the trading markets. The Securities and Exchange Commission (SEC) has proposed more comprehensive compliance requirements for digital asset exchanges. The core of the requirements is reflected in the restrictions of offering digital assets trading service.

- In the last two years, the SEC has reiterated on many occasions that digital assets that have characteristics of a security should not be traded on a digital asset exchange

In August 2017, when the development of ICO was at its peak, the SEC issued an investor bulletin “Investor Bulletin: Initial Coin Offerings” on its website and published an investigation report of the DAO. It determined that the DAO tokens were considered ‘marketable securities’, stressing that all digital assets considered ‘marketable securities’ would be incorporated into the SEC regulatory system, bound by the U.S. federal securities law. Soon after, the SEC also declared and stressed that “(if) a platform offers trading of digital assets that are securities and operates as an “exchange,” as defined by the federal securities laws, then the platform must register with the SEC as a national securities exchange or be exempt from registration.”

On 16 November 2018, the SEC issued a “Statement on Digital Asset Securities Issuance and Trading,” in which the SEC used five real case studies to conduct exemplary penalty rulings on the initial offers and sales of digital asset securities, including those issued in ICOs, relevant cryptocurrency exchanges, investment management tools, ICO platforms and so on. The statement further reiterates that exchanges cannot provide trading services for digital assets that have characteristics of a security.

On 3 April 2019, the SEC issued the “Framework for ‘Investment Contract’ Analysis of Digital Assets” to further elucidate the evaluation criteria for determining whether a digital asset is a security and providing guiding opinions on the compliance of the issuance, sales, holding procedures of digital assets.

- As of now, only a small number of digital assets, such as BTC, ETH, etc. meet the SEC’s requirement of “non-securities assets.” The potentially “compliant” digital assets are less than 20.

Early in March 2014, the Inland Revenue Service (IRS) has stated that Bitcoin will be treated as a legal property and will be subject to taxes. In September 2015, the U.S. Commodity Futures Trading Commission (CFTC) stated that Bitcoin is a commodity and will be treated as a “property” by the IRS for tax purposes.

On 15 June 2018, William Hinman, Director of the Corporate Finance Division of the SEC, said at the Cryptocurrency Summit held in San Francisco that BTC and ETH are not securities. Nevertheless, many ICO tokens fall under the securities category.

So far, only BTC and ETH have received approval and recognition of the U.S. regulatory authority as a “non-securities asset.”

Since July 2018, the SEC has investigated more than ten types of digital assets, one after another, and ruled that they were securities and had to be incorporated into the SEC regulatory system. It prosecuted and punished those who had contravened the issuance and trading requirements of the securities laws.

Although there are still many digital assets that have yet to be characterised as “securities”, it is extremely difficult to be characterised as a “non-securities asset” based on the evaluation criteria announced by the SEC. As the SEC’s spokesperson has reiterated many times, they believe the majority of ICO tokens are securities.

Under the stipulated requirements of the SEC, Coinbase, a leading U.S. exchange, has withdrawn a batch of digital assets. The assets withdrawn included digital assets that had been characterised as “securities” as well as those that have high risks of being characterised as “securities.” However, it is worth noting that although the risk to be characterised as “securities” for more than ten types of digital assets, which have not been explicitly required by SEC to be withdrawn, is relatively small, they are not entirely safe. With the further escalation of the SEC’s investigations, they could still be characterised as securities and be held accountable for violating their responsibilities. However, this requires further guidance from the SEC.

*Coinbase’s 14 types of digital assets that have yet to be requested for withdrawal

Poloniex announced on 16 May that it would stop providing services for nine digital assets, including Ardor (ARDR), Bytecoin (BCN), etc. under the compliance guidelines of the SEC. On 7 June, Bittrex also announced that it would stop providing trading services to U.S. users for 32 digital assets. The action of the SEC on its regulatory guidance was further reinforced apparently.

In fact, it is not the first time that these two exchanges have withdrawn digital assets under regulatory requirements. Since the rapid development of digital assets driven by ICO in 2017, Poloniex and Bittrex were once leading exchanges for ICO tokens, providing comprehensive trading services for digital assets. However, after the SEC reiterated its compliance requirements, Poloniex and Bittrex have withdrawn a considerable amount of assets in the past year to meet the compliance requirements.

In conclusion, the takeaways that we have got are as follows: Under the existing U.S. regulatory requirements of digital assets, after obtaining the basic entry licences (MSB, MTL), exchanges could either choose the “compliant asset” solution of Coinbase and only list a small number of digital assets that do not have apparent characteristics of a security, and at all times prepare to withdraw any asset later characterised as “securities” by the SECs; or choose to be like OKEx and Huobi and make it clear they would “not provide services to any U.S. users” at the start.

Binance has been providing a large number of digital assets that have characteristics of a security to U.S users without a U.S. securities exchange licence, so it has already contravened the SEC regulatory requirements.

On top of that, it is also worth noting that the rapid development of Binance has been achieved precisely through the behaviours of “contrary to regulations” and “committing crimes.” Amid the blocking of several pioneering exchanges, such as OKCoin, Huobi, etc. providing services to Chinese users in the Chinese market under new laws from the regulatory authorities, Binance leapfrogged the competition and began to dominate the Chinese market. Similarly, Binance’s rapid growth in the U.S. market is mainly due to its domination of the traffic of digital assets withdrawn by Poloniex and Bittrex. One can say that Binance not only has weak awareness of compliance issues, but it is also indeed “playing with fire” with the U.S. regulators.

In April 2018, the New York State Office of Attorney General (OAG) requested 13 digital asset exchanges, including Binance, to prepare for investigations, indicating it would initiate an investigation in relations to company ownership, leadership, operating conditions, service terms, trading volume, relationships with financial institutions, etc. Many exchanges, including Gemini, Bittrex, Poloniex, BitFlyer, Bitfinex, and so on, proactively acknowledged and replied in the first instance upon receipt of the investigation notice. However, Binance had hardly any action.

Binance has been illegally operating in the U.S. for almost two years. It has not yet fulfilled the FinCEN and MSB registration requirements. Moreover, it has also neglected the SEC announcements and OAG investigation summons on several occasions. The ultimate announcement of exiting the U.S. market may be due to the tremendous pressure imposed by the U.S. regulators.

In fact, the SEC executives have recently stressed that “exchanges of IEO in the U.S. market are facing legal risks and the SEC would soon crack down on these illegal activities” on numerous occasions. These were clear indications of imposing pressure on Binance.

Regarding the SEC’s rulings on illegal digital asset exchanges, EtherDelta and investment management platform, Crypto Asset Management, it may not be easy for Binance to “fully exit” from the U.S. market. It may be faced with a hefty penalty. Once there are any compensation claims by the U.S. users for losses incurred in the trading of assets at Binance, it would be dragged into a difficult compensation dilemma. It would undoubtedly be a double blow for Binance that has just been held accountable for the losses incurred in a theft of 7,000 BTC.

Coincidentally, Binance was tossed out of Japan because of compliance issues. In March 2018, the Financial Services Agency of Japan officially issued a stern warning to Binance, which was boldly providing services to Japanese users without registering for a digital asset exchange licence in Japan. Binance was forced to relocate to Malta instead. Binance may have to bear hefty penalties arising from challenging the compliance requirements after it had lost important markets due to consecutive compliance issues.

The rise of Binance was attributed to its bold and valiant style, grasping the opportunity created in the vacuum period of government regulation, breaking compliance requirements and rapidly dominating the market to obtain user traffic. For a while, it gained considerable advantages in the early, barbaric growth stage of the industry. Nonetheless, under the increasingly comprehensive regulatory compliance system for global digital asset markets, Binance, which has constantly been “evading regulation” and “resisting supervision” would undoubtedly face enormous survival challenges, notwithstanding that it would lose far more than 50 per cent of the market share.

/(CBDC) Guide")